One of the many things that you will need to consider when preparing your estate plan is how you would like your personal effects to be distributed. Almost everyone has an item of special meaning that they would like distributed to a certain person. Traditionally, these requests were included in the Last Will and Testament or the revocable trust documents. The disadvantage to this method was that whenever you wanted to make a change, whether it be changing the item or the recipient, or adding additional items, you had to sign a codicil to your Will or an amendment to your revocable trust. This would incur additional costs because the Codicil or the amendment had to be executed with the same formalities as the Will or revocable trust, which usually meant a trip to the attorney’s office.

How to Protect Your Disabled Loved One with a Special Needs Trust

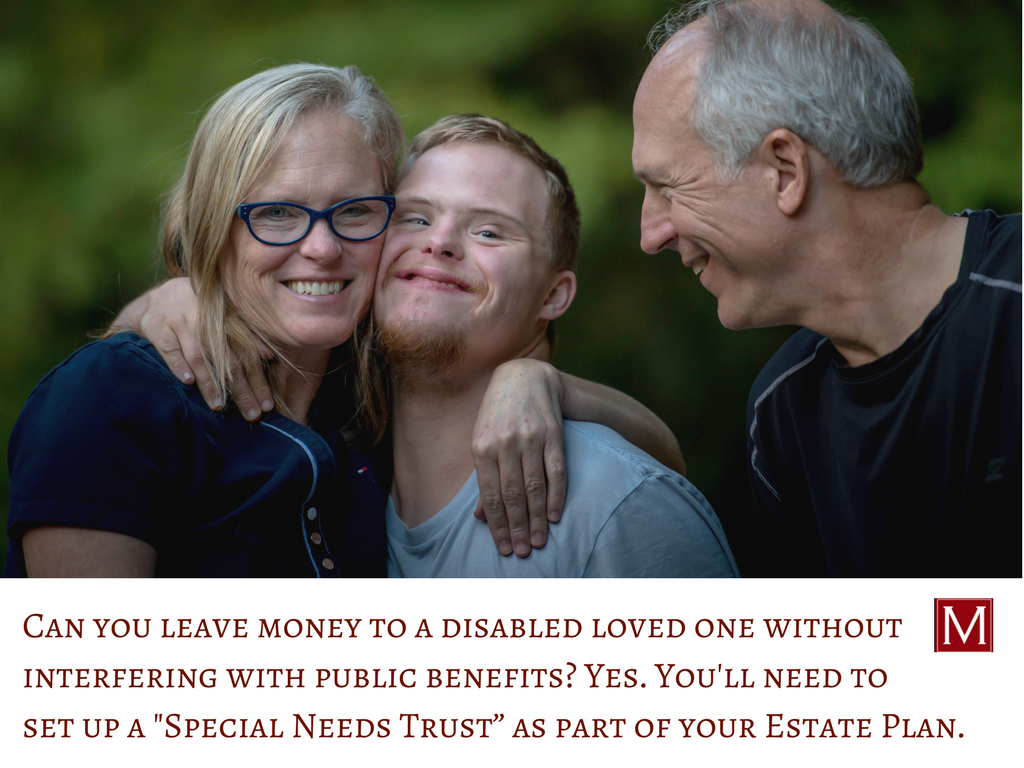

Have you been told that you cannot leave money to a disabled son, daughter, or grandchild? If they receive certain Government benefits, it’s true. Fortunately, there is a solution to this problem. Read on to understand how a Special Needs Trust is in your loved one’s best interest. Learn how to plan carefully so you’re not jeopardizing your loved one’s ability to receive Supplemental Security Income (SSI) and Medicaid benefits.

What Government Benefits Have Asset Restrictions?

Benefits that have asset restrictions include Supplemental Security Income (SSI), Medicaid, and subsidized housing. Unfortunately, if the individual has more than the maximum amount, his or her benefits will be interrupted. If you want to leave money upon your death or a gift during your lifetime to someone with a physical or mental disability, or a person who is chronically ill, you must know your legal rights and plan carefully. How have I been able to protect my clients? By helping them set up a Special Needs Trust as part of their estate plan.

What is a Special Needs Trust?

You can leave money to your loved one without interfering with the public benefits by setting up a Special Needs Trust (also referred to as a Supplemental Needs Trust). This type of trust enables a person with a disability or chronic illness to have an unlimited amount of assets held for his or her benefit. That being said, instead of leaving property directly to your loved one, you leave it to this trust. The assets held in the trust as not considered “countable” assets in determining whether the individual qualifies for the benefits because the individual does not own them, rather the trust does. The trust, in turn, provides for extra items or care over and above what the government provides.

How Can the Trust Be Used?

The Special Needs Trust can pay for many of the items or services your loved one may want or need in the future. For example, Medicaid won’t pay for certain a medical treatment, the trust can step in and pay for it. If Medicaid will only pay for a basic piece of medical equipment, the trust can provide whatever additional funds are necessary to pay for a nicer model. The trust can pay for alternative treatments, vitamins and supplements, massages and even grooming supplies. The Trust can also pay for those extras that may not be medically necessary, but which would definitely increase the disabled person’s quality of life, such as summer camp, airline tickets for travel (including a companion, if necessary), electronic games, computer equipment, nicer furniture or even a larger television.

What Assets Can Be Used to “Fund” A Special Needs Trust?

Almost any type of asset can be used to “fund” a special needs trust, including life insurance proceeds, other inheritances or lifetime gifts. Once the trust is established, other family members or friends can add to the trust through their own estate plans.

Who Manages the Trust?

The trust funds are managed, administered and distributed by the trustee. The trustee should be someone who gets along well with the disabled person and has his best interests at heart as he is the one who will decide if and when any money is distributed. The trustee should also be someone who is comfortable managing money and has a track record of being responsible with their own money.

If you do not have a good candidate to serve as trustee, or if you intend to leave only a modest amount of money to the trust, consider using a “pooled trust.” A pooled trust is a type of special needs trust that is run by a non-profit organization which pools and invests funds from many families. Under the pooled trust structure, each disabled person still has a separate account for those funds added by his family which are used only for his benefit, but all of the funds are invested and managed as a whole.

Additional Benefits of a Special Needs Trust

While it may seem like a good idea simply to leave a set amount of money to a sibling or other close relative, with the understanding that the money will be spent on the disabled person, this strategy often backfires. Once the “holder” receives the money, it legally belongs to him, and he cannot be forced to use it for the disabled person. Even when all the parties have the best of intentions, things can still go wrong. If the “holder” of the money passes away, those funds will be distributed to his or her beneficiaries, who may not want to use it for the disabled person. The “holder” may at some later point in time be involved in litigation, bankruptcy or a divorce. None of those legal proceedings would differentiate between the money he is “holding” for the benefit of the disabled person and his own assets.

The use of a Special Needs Trust would solve these problems while ensuring that the funds are used solely to enrich the life of the disabled person.

Let’s Connect.

If you’d like to learn more or set up a Special Needs Trust as part of your estate plan, let’s talk. You can reach me by clicking below.

What You Need to Settle Your Affairs

A Checklist of Documents You Will Need to Settle Your Affairs After You Die

• List of Funeral Instructions and prepaid funeral contracts

• Medicare Card/Health Insurance Card

• VA File Number, Military discharge papers

• Birth certificate and Death Certificate

• Marriage license or Divorce Decree

• Prenuptial/postnuptial agreements

• Revocable/Living Trust agreements

• Last Will and Testament

What is a Trust?

Trusts: An Explanation of What They Are and How They Could Benefit You

A trust is a legal relationship in which one person, the Grantor, transfers property to another person known as the Trustee. The Trustee then holds the property, managing and using it for the benefit of a third person, known as the beneficiary. The property can be almost any type of property- money, real estate, business interests, securities, etc. The Grantor may also be referred to as the Donor, Settlor or Trustor. Depending upon the type of trust, the Grantor, Trustee and Beneficiary may be three different individuals, or in some instances, they may all be the same person. The document which creates this relationship and spells out the terms is known as the “trust agreement.” Once created, a trust is a legal entity which is capable of owning property. It may even have its own tax payer identification number and have to file income tax returns.

Organizing Your Most Important Papers

One thing each of us can do for the future is to get our personal and financial records in order. These records are both useful and something you will need on numerous occasions throughout your lifetime, including annual income tax preparation, financial planning and estate planning. It may even be relatives or friends who will need it in the event that something has happened to you. If you become incapacitated or pass away, your loved ones will need this information and documentation to take over your financial affairs, deal with insurance claims, apply for government benefits (such as medical assistance), or to settle your personal and financial affairs in the event of your death. You’re doing your loved ones a tremendous favor by keeping good records. Your filing system doesn’t need to be elaborate, just organized. The following is a list of what records you should maintain and how long you should maintain them.

When a Loved One Dies

A Checklist of What to Do When a Loved One Dies

When a loved one passes away, it is an understandably stressful time. It can be even more stressful and/or traumatic trying to remember all of the details that must be taken care of related to a person’s death. If you are in charge of handling the affairs of the decedent (the person who has died), here is a checklist of some of the more important considerations: